by administrator | Apr 17, 2026 | Blogs

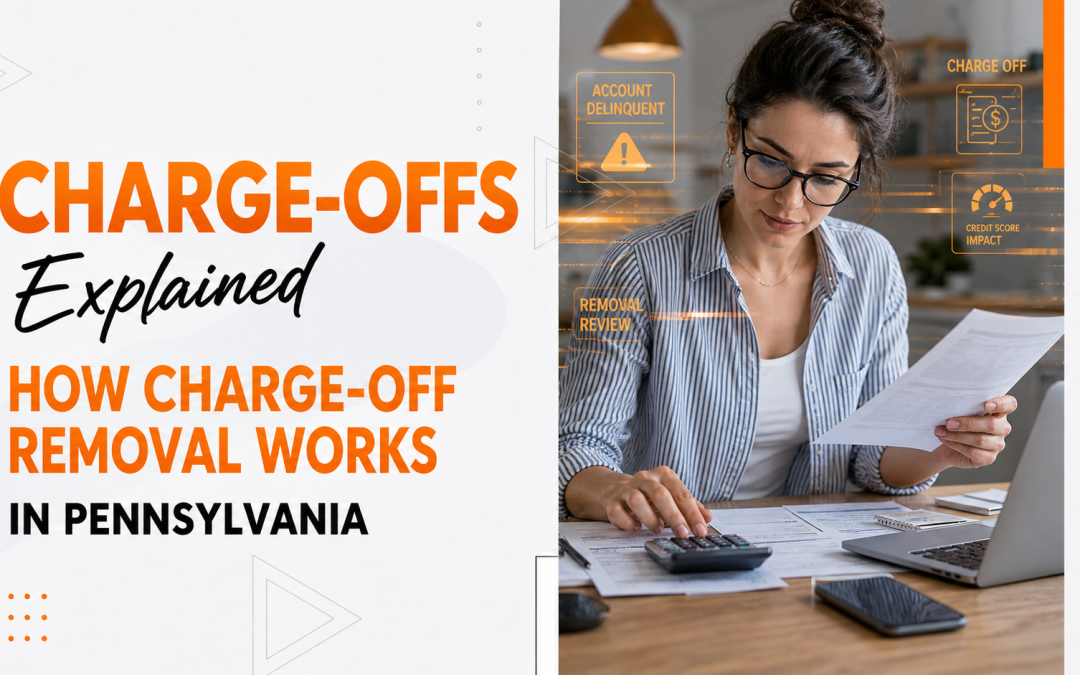

Many consumers misunderstand charge-offs. A charge-off can damage your credit report, lower your credit score, and make lenders view you as a higher-risk borrower. Many people in Pennsylvania mistakenly believe that once an account is “charged off,” the debt is gone. In reality, a charge-off signals a serious missed payment, negatively impacting your credit score and staying on your report for years.

It’s important to know how charge-offs work, how they show up on your credit report, and when charge-off removal in PA might be possible if you want to fix or rebuild your credit. Not every charge-off can be removed, but many are reported incorrectly or in violation of credit reporting rules.

In the following sections, you’ll learn what charge-offs are, how they affect people in Pennsylvania, how to dispute them, common mistakes to watch out for, and ways to rebuild your credit after dealing with charge-offs.

What Is a Charge-Off and How Does It Appear on Your Credit Report?

A charge-off occurs when a creditor determines a debt is unlikely to be paid and records it as a loss, usually after 180 days of nonpayment on a revolving account. This step helps the creditor, not the consumer.

Key Facts About Charge-Offs:

- You still owe the debt, even after it is charged off.

- The account remains on your credit report.

- The creditor may continue collection efforts.

- The debt may be sold to a collection agency.

- A charge-off can appear alongside a collection for the same debt.

On a credit report, a charge-off is usually labeled as:

- “Charged off”

- “Charge-off / bad debt”

- “Profit and loss write-off”

Since charge-offs indicate that payments have been missed for an extended period, lenders view them as a strong warning sign.

How Charge-Offs Impact Credit Scores and Lending Decisions

Charge-offs significantly affect credit because they directly impact payment history, the most influential credit scoring factor.

How Charge-Offs Damage Credit:

- Causes substantial credit score drops.

- Signal high risk to lenders

- Reduce the odds of loan and credit card approvals.

- Increase interest rates

- Complicated housing and employment screenings.

Recent charge-offs hurt your credit most, but older ones can also impact loan approvals, especially for cars or mortgages.

If you live in Pennsylvania and have multiple charge-offs, it can make it much harder to move forward financially unless you handle them properly.

Common Charge-Off Reporting Errors Seen in Pennsylvania

Creditors and collectors often report charge-offs with mistakes. Because of this, many Pennsylvania consumers dispute charge-offs when they find wrong dates, balances, duplicate accounts, or incomplete account details.

Common Errors Include:

- Incorrect charge-off dates

- Wrong balances reported

- Accounts reported as charged off when they were settled

- Duplicate reporting after debt sale

- Charge-offs reported beyond the legal time limit.

- Inconsistent reporting across credit bureaus

- Missing or incomplete account information

Can Charge-Offs Be Removed From Credit Reports in Pennsylvania?

You can’t remove a charge-off just because it’s negative, but you can get it removed or fixed if it’s wrong, missing information, or cannot be verified.

Charge-Offs May Be Disputed If:

- The account information is incorrect.

- The balance does not match the creditor records.

- The dates are inaccurate.

- The creditor cannot verify the account.

- Reporting violates credit laws.

- The account is duplicated or misclassified.

To dispute a wrong charge-off on your credit report, you need to review your records carefully, gather proof, and follow the right steps.

How to Dispute Charge-Offs in Pennsylvania: Step-by-Step

Disputing a charge-off is harder than fixing small mistakes, so it’s important to be careful.

Step 1: Review All Credit Bureau Reports

Step 2: Identify Specific Errors

Focus on factual inaccuracies rather than the existence of the debt itself.

Step 3: Gather Supporting Documentation

Helpful documentation may include:

- Payment records

- Settlement agreements

- Account statements

- Correspondence with creditors

Step 4: Submit Strategic Disputes

Step 5: Review Investigation Results

If the creditor can’t prove the account details are correct, the charge-off might be fixed or removed.

You need to be both persistent and accurate when disputing charge-offs.

Paying a Charge-Off vs. Disputing It: What PA Consumers Should Know

Many consumers rush to pay charge-offs without understanding the consequences.

Important Considerations:

- Paying a charge-off does not remove it.

- Paid charge-offs may still affect credit.

- Payment can update the account and change the scoring impact.

- Negotiations should be approached carefully.

Often, it’s best to check if the charge-off is reported correctly before deciding to pay it.

Common Mistakes Consumers Make With Charge-Offs

You need a plan to handle charge-offs, because mistakes can make things worse.

Common Errors Include:

- Paying charge-offs without reviewing the reporting

- Disputing without evidence

- Ignoring sold or transferred debts

- Closing accounts incorrectly

- Believing charge-offs mean the debt is gone.

If you avoid these mistakes, you’ll have a better chance of fixing your credit.

How to Rebuild Credit After Charge-Offs Are Addressed

No matter if a charge-off is fixed, removed, or still on your report, it’s important to work on rebuilding your credit.

Effective Rebuilding Strategies:

- Maintain a perfect payment history going forward.

- Keep balances low

- Add positive trade lines carefully.

- Avoid unnecessary inquiries

- Monitor credit reports consistently.

Good credit habits can help lessen the long-term effects of charge-offs.

Conclusion: Taking Control of Charge-Offs in Pennsylvania

Charge-offs can feel overwhelming, but you still have options. If you live in Pennsylvania, understanding how charge off removal PA works can help you protect your credit and make better financial decisions.

Start by reviewing your credit reports, identifying inaccurate information, gathering proof, and submitting clear disputes. If a creditor or collector reports wrong, outdated, duplicate, or unverifiable information, the credit bureau may need to correct or remove it.

Some consumers handle disputes on their own. Others choose professional help, especially when they have multiple charge-offs, confusing account histories, or repeated reporting errors.

Credit Repair Associates helps Pennsylvania consumers review inaccurate charge-offs, dispute credit reporting errors, and rebuild credit with confidence.

Frequently Asked Questions About Charge-Off Removal in PA

Does paying a charge-off remove it from my credit report?

No. Payment alone does not guarantee removal.

How long do charge-offs stay on credit reports?

Are charge-offs worse than collections?

Often yes, especially if recent.

Can I dispute a charge-off myself?

Yes, consumers have the legal right to dispute inaccurate reporting.

References

Reference (On This site)

How to Dispute Credit Report Errors in Philadelphia: A Local Consumer’s Guide

by administrator | Apr 3, 2026 | Blogs

Late payments are the most common negative marks on credit reports and can do a lot of harm. Just one missed or late payment can lower your credit score and stay on your report for years.

Knowing how late payment credit repair works is important if you want to improve your credit. Not every late payment can be removed, but some are reported by mistake or unfairly. Others can be managed by rebuilding your credit over time.

This guide explains how late payments show up on credit reports, how they affect your score, when you can dispute them, mistakes to watch out for, and ways to rebuild your credit.

What Is a Late Payment and How Is It Reported?

A late payment happens when you miss a payment by its due date. Most lenders give you a short grace period, but if your payment is 30 days late, it can be reported to the credit bureaus.

How Late Payments Appear on Credit Reports:

- 30 days late

- 60 days late

- 90 days late

- 120+ days late

The longer a payment is overdue, the more it can hurt your credit score.

Late payments may be reported on:

- Credit cards

- Auto loans

- Mortgages

- Student loans

- Personal loans

How Late Payments Affect Credit Scores and Lending Decisions

Effects of Late Payments Include:

- Immediate credit score drops

- Increased perceived risk to lenders

- Higher interest rates

- Lower approval odds

- Difficulty qualifying for housing or refinancing

If you have good credit, a late payment can cause a sudden and big drop in your score.

Common Late Payment Reporting Errors Consumers Overlook

Many people think late payments on their credit report are always correct, but mistakes happen more often than you might think.

Common Late Payment Errors Include:

- Payments reported late despite on-time payment

- Payments misapplied to the wrong billing cycle

- Payments reported late during deferment or forbearance

- Late payments reported after account closure

- Inconsistent reporting across credit bureaus

- Duplicate late payment entries

These mistakes can unfairly hurt your credit, but you can dispute them.

When Late Payments Can Be Disputed and Potentially Removed

You can’t remove late payments just because they hurt your credit. But if they are wrong, incomplete, or can’t be verified, you can dispute them.

Late payments may be disputed if:

- Payment was made on time

- Creditor failed to credit the payment properly

- Account was in deferment or hardship status

- Payment history is inconsistent across bureaus

- Account information is incomplete or incorrect

To dispute a wrong late payment, you’ll need proof and clear communication.

How Late Payment Credit Repair Works: Step-by-Step

Be careful when disputing late payments so your request isn’t rejected.

Step 1: Review All Credit Reports

Step 2: Identify Specific Errors

Focus on factual inaccuracies rather than the missed payment itself.

Step 3: Gather Supporting Documentation

Useful documents may include:

Bank statements

Payment confirmations

Billing statements

Hardship or deferment agreements

Step 4: Submit Disputes Strategically

Writing out your dispute can clarify your case when dealing with late payment issues.

Step 5: Review Results and Follow Up

If your dispute is denied, you might need to send more proof or take your case to a higher level.

Paying On-Time Going Forward: Why Rebuilding Matters More Than Removal

Even if late payments stay on your report, you can still rebuild your credit successfully.

Rebuilding Strategies Include:

- Making all payments on time going forward

- Keeping credit utilization low

- Avoiding unnecessary credit inquiries

- Maintaining older accounts

- Adding positive trade lines cautiously

As you keep up good credit habits, late payments will matter less over time.

Common Mistakes Consumers Make With Late Payment Credit Repair

Late payment credit repair requires both patience and strategy.

Common Errors Include:

- Disputing accurate late payments repeatedly

- Closing old accounts with a positive history

- Ignoring utilization and balances

- Falling for “guaranteed removal” promises

Steering clear of these mistakes will help you keep improving your credit.

When Professional Help May Be Appropriate

Sometimes, late payment issues are more complicated.

Professional Help May Be Helpful If:

- Late payments are reported inaccurately

- Multiple bureaus show inconsistent data

- Hardship programs were not honored

- Credit repair efforts are stalled

Conclusion: Moving Forward After Late Payments

Late payments can feel discouraging, but they don’t decide your financial future. Learning about late payment credit repair helps you take control, whether you dispute errors, rebuild your credit, or get professional help.

Frequently Asked Questions About Late Payments on Credit Reports

Can late payments be removed from credit reports?

Only if they are inaccurate, incomplete, or unverifiable.

How long do late payments stay on credit reports?

Up to seven years from the date of delinquency.

Do late payments affect credit forever?

No. Their impact decreases over time with positive behavior.

Can I dispute late payments myself?

Yes. Consumers have the legal right to dispute at no cost.

References

Reference (On This Site)

Credit Repair Pennsylvania: The Complete Guide to Fixing, Understanding, and Improving Your Credit

by administrator | Mar 20, 2026 | Blogs

Identity theft can ruin your credit profile in just a few days or weeks. In a busy city like Philadelphia, where data breaches, stolen mail, and online scams happen often, identity theft is a real threat to your finances. Many people only find out after they are turned down for credit, housing, or a job.

If you want to fix your credit and protect yourself from future problems, it’s important to understand how identity theft credit repair works in Philadelphia. Repairing your credit after identity theft means more than just filing disputes. You’ll need to gather documents, understand your legal rights, and monitor your credit over time.

This guide will show you how identity theft appears on credit reports, what steps to take right away, how to handle disputes, mistakes to avoid, and when to get professional help to speed up your recovery.

What Is Identity Theft and How Does It Appear on Credit Reports?

Identity theft happens when someone uses your personal information, like your Social Security number, name, or date of birth, without your permission to open accounts, get loans, or commit fraud.

Common Signs of Identity Theft on Credit Reports:

- Accounts you don’t recognize

- Unauthorized hard inquiries

- Incorrect personal information

- Sudden drops in credit scores

- Collections tied to unfamiliar accounts

- Address or employer changes you didn’t make

Credit bureaus update your information all the time, so if you don’t act fast, fraud can show up on all three of your credit reports very quickly.

Why Identity Theft Is Especially Disruptive for Philadelphia Consumers

Philadelphia consumers face unique challenges related to identity theft, including:

- High population density leading to mixed credit files

- Medical identity theft from hospital billing systems

- Stolen mail or package theft

- Increased digital fraud in urban areas

- Rental-related identity misuse

Because of these issues, you might end up with several fake accounts across different credit reports, making the problem harder to fix and taking longer to resolve.

Immediate Steps to Take After Discovering Identity Theft

Step 1: Place Fraud Alerts or Credit Freezes

Step 2: Review All Credit Reports

Look at your credit reports from Equifax, Experian, and TransUnion to spot any signs of fraud.

Step 3: File an Identity Theft Report

Step 4: Contact Affected Creditors

Let your lenders and any collection agencies know about the fraud as soon as possible.

Acting quickly helps limit further credit damage.

How Credit Report Identity Theft Disputes Work

What Can Be Disputed:

- Fraudulent accounts

- Unauthorized inquiries

- Incorrect balances tied to fraud

- Collections resulting from identity theft

Supporting Documentation May Include:

- Identity theft reports

- Police reports (when applicable)

- Affidavits of fraud

- Proof of identity

Once you file your disputes, the credit bureaus have to look into them and remove any fraudulent information they can’t verify.

Common Identity Theft Credit Repair Mistakes to Avoid

Recovering from identity theft requires attention to detail.

Common Mistakes Include:

- Delaying action

- Disputing fraud without documentation

- Failing to place credit freezes

- Ignoring follow-up notices

- Assuming one dispute fixes everything

Avoiding these mistakes speeds up recovery and prevents repeat damage.

How Long Does Identity Theft Credit Repair Take

Recovery timelines for identity theft can range from a few weeks to several months, depending on the complexity of the case.

Typical Factors Affecting Timeline:

- Number of fraudulent accounts

- Bureau responsiveness

- Documentation completeness

- Ongoing fraudulent activity

Most people begin to see progress within 30 to 90 days after taking action. However, if your case involves many fraudulent accounts or ongoing fraud, it may take six months or longer to fully restore your credit.

Rebuilding Credit After Identity Theft Is Resolved

Once the fake accounts are gone, it’s important to start rebuilding your credit.

Rebuilding Strategies Include:

Rebuilding your credit helps you get back on track and makes your finances stronger for the future.

When Professional Identity Theft Credit Repair Help Makes Sense

Dealing with identity theft is usually more complicated than fixing regular credit problems.

Professional Help May Be Best If:

- Multiple fraudulent accounts exist.

- Identity theft reoccurs

- Collections or lawsuits are involved.

- Credit bureaus deny valid disputes.

- You lack time or documentation confidence.

Professional credit repair services understand how to escalate your case and use legal protections to help you recover.

Conclusion: Restoring Credit After Identity Theft in Philadelphia

Identity theft is stressful, but it doesn’t have to ruin your finances forever. By learning about identity theft

credit repair in Philadelphia, you can act fast, protect your rights, and rebuild your credit.

Credit report identity theft can affect consumers across Philadelphia, including Center City, South Philadelphia, West Philadelphia, Northeast Philadelphia, Germantown, Kensington, and surrounding areas. Because fraudulent credit activity can impact housing, car loans, personal loans, and employment screenings, local consumers should address suspicious credit report activity as soon as possible.

If you’re in Philadelphia and facing a tough identity theft case, don’t wait—

reach out to Credit Repair Associates today. Our expert team specializes in disputing fraudulent accounts, guiding you step by step through your recovery, and helping you restore your financial confidence so you can move forward with peace of mind. Take control of your credit now and get the support you deserve.

Frequently Asked Questions About Identity Theft and Credit Reports

Can identity theft accounts be removed from credit reports?

Yes, when properly documented and disputed.

Will identity theft permanently damage my credit?

No. With action, credit can be restored.

Should I file a police report?

It can strengthen disputes, especially for serious cases.

Can I handle identity theft credit repair myself?

Yes, but professional help can simplify complex cases.

References

Reference (On this site)

How to Dispute Credit Report Errors in Philadelphia: A Local Consumer’s Guide

by administrator | Feb 15, 2026 | Blogs

Philadelphia is a city of neighborhoods—Fishtown, West Philly, Germantown, South Philly—each with its own vibe. But when it comes to your credit, the rules are the same everywhere: accuracy matters, and errors can quietly cost you real money.

If you’ve spotted Philadelphia credit report errors—a late payment you swear you didn’t miss, a collection account that isn’t yours, a medical bill you already paid—this guide will walk you through how to dispute credit report errors in Philadelphia in a way that’s organized, evidence-based, and designed to get results.

You’ll learn:

-

Why credit accuracy affects far more than loans

-

Your FCRA credit report dispute rights

-

The credit bureau dispute process from start to finish

-

How to handle tough categories like medical collections dispute, mixed credit file dispute, and identity theft credit report dispute

-

Exactly how long do credit report disputes take, and what to do if you get a “verified” response

Why Disputing Philadelphia Credit Report Errors Matters (and How It Impacts Your Score)

A lot of people assume “credit repair” is only about removing negative items. In reality, the most consumer-friendly starting point is simply making your reports accurate. When you dispute credit report errors in Philadelphia, you’re not asking for a favor—you’re using your legal right to correct information that can affect your financial life.

Why errors hurt more than you think

A credit report is used to build your credit scores and to evaluate you for major life decisions. In Philadelphia, inaccurate reporting can affect:

-

Apartment applications (many Philly landlords screen credit)

-

Utility deposits (a lower score can trigger larger deposits)

-

Insurance pricing (in many states, credit-based insurance scores can matter)

-

Auto financing (rates can change dramatically with score tiers)

-

Employment screenings for certain roles (credit report checks may be used where permitted)

Even one wrong late payment can lower a score and increase your borrowing costs. A single collection—especially if it’s inaccurate—can be the difference between “approved” and “denied.”

Credit repair, explained simply

Think of credit repair as a three-part process:

-

Review your reports for accuracy and red flags

-

Dispute incorrect or unverifiable items using documentation

-

Rebuild with smart credit habits so your score benefits long-term

This guide focuses heavily on the dispute side, because that’s where many consumers get stuck or waste time.

The Philly-specific reality: high-volume reporting errors happen

Philadelphia has large hospital systems, lots of rental turnover, and the same national banks and collectors as everywhere else—meaning data moves fast. When accounts change hands (especially collections), mistakes happen: wrong balances, wrong dates, wrong consumers, duplicate accounts, or outdated statuses.

Bottom line: if you see Philadelphia credit report errors, doing nothing is usually the most expensive option. A smart credit report dispute Philadelphia plan can protect your score now and reduce stress later.

Know Your FCRA Credit Report Dispute Rights Before You Start

Before you send a single form, it helps to understand the rules that control the credit bureau dispute process. The primary law here is the Fair Credit Reporting Act (FCRA).

Your core FCRA dispute rights (the consumer-friendly version)

Under the FCRA, you generally have the right to:

-

Dispute information you believe is inaccurate or incomplete

-

Have the credit bureau investigate your dispute

-

Receive results and an updated report if changes are made

-

Have corrected information shared with other bureaus in certain situations

The key is to dispute in a way that makes it easy to investigate—clear explanation + evidence.

How long do credit report disputes take?

This is one of the most common questions: how long do credit report disputes take?

In many cases, bureaus have about 30 days to investigate, and the timeline can extend to 45 days in certain situations (for example, depending on how you obtained the report or if you add new information during the investigation window). The CFPB explains these timelines and the common reasons for extensions.

The CFPB also notes that disputes submitted to credit reporting agencies generally require 30–45 days for a response, and encourages consumers to allow that process to play out before filing a CFPB complaint too early.

What the bureaus actually do during an investigation

When you file a dispute, the bureau typically:

-

Logs your dispute and identifies the data furnisher (the company reporting)

-

Sends the furnisher a request to verify or correct data

-

Updates, deletes, or keeps the item based on results

-

Notifies you of the outcome

If you’ve ever gotten a frustrating “verified” response, it often means the furnisher confirmed the data as they have it—not necessarily that it’s truly correct. That’s why documentation and follow-up strategy matter (we’ll cover this in Section 6).

The biggest mindset shift: you’re building a case file

A successful dispute isn’t about emotion (“I’m upset”). It’s about clarity:

That “mini case file” approach is how consumers create leverage and reduce back-and-forth—especially when they want to dispute errors with Equifax Experian TransUnion efficiently.

Step-by-Step: How to Dispute Credit Report Errors in Philadelphia (The Right Way)

If you’ve been wondering how to dispute credit report in Philadelphia, here’s the practical blueprint—organized, repeatable, and designed to keep you from making the most common mistakes.

Step 1: Pull fresh reports (all three bureaus)

Start by getting your reports from:

-

Equifax

-

Experian

-

TransUnion

Compare them line by line. The same account can appear differently across bureaus, so you want to spot inconsistencies.

Tip: Print or save PDFs of the reports you’re disputing. Your dispute should reference exactly what you saw on a specific date.

Step 2: Identify the dispute category (this changes your strategy)

Common dispute categories include:

-

Wrong personal info (name variations, addresses, employers)

-

Accounts not yours (possible identity theft or mixed file)

-

Incorrect late payments

-

Duplicate collections

-

Wrong balances or limits

-

Collections that should show paid/settled

-

Medical collections issues (more in Section 4)

Step 3: Gather proof before you submit

Your dispute is stronger when you attach supporting documents. Examples:

-

Bank statements or proof of payment

-

Billing statements showing correct dates

-

Letters from creditors confirming changes

-

Police report / IdentityTheft.gov report for identity theft

-

Insurance EOBs (for medical disputes)

-

Any court documentation (if relevant)

Step 4: Choose your dispute method (online vs mail)

You can dispute online, by phone, or by mail. Many consumers prefer mail for serious disputes because it creates a cleaner paper trail.

If you mail:

-

Use certified mail with return receipt

-

Include copies (not originals) of documents

-

Keep a complete packet copy for yourself

Step 5: Dispute with the bureau(s) where the error appears

If the error shows on all three reports, you may need to dispute errors with Equifax Experian TransUnion separately (each bureau maintains its own file).

Bullet-point structure for what to include:

-

Your identifying info (full name, DOB, partial SSN)

-

The specific item being disputed (creditor name, account number partial, date reported)

-

What’s wrong and why (1–3 sentences)

-

What you want: delete, correct, update status, correct dates

-

Your supporting documents list

Step 6: Track the clock and responses

Because how long do credit report disputes take can vary, set reminders:

Step 7: Review results like an auditor

When you receive the outcome, ask:

-

Was the item deleted, corrected, or “verified”?

-

Did the bureau fix it on all bureaus or only one?

-

Did the furnisher update the same error elsewhere?

This is the backbone of a strong credit report dispute Philadelphia workflow—organized evidence, clear requests, and follow-through.

What to Dispute and How: Collections, Medical Bills, Mixed Files, and More

Not all disputes are equal. Some items are quick fixes; others need a more strategic approach. Below are the most common “high-impact” categories Philadelphia consumers run into, plus how to dispute each one.

A) How to dispute an inaccurate collection account

If you need to dispute inaccurate collection account reporting, focus on the facts that are easiest to verify:

-

Is the balance wrong?

-

Are the dates wrong (date of first delinquency, opened date)?

-

Is it duplicated (same debt listed twice)?

-

Is it reporting under the wrong consumer?

Actionable tips:

-

Ask the bureau to investigate accuracy and completeness

-

Attach proof of payment or settlement terms if you have them

-

If the account isn’t yours, don’t “explain” too much—keep it direct and evidence-based

B) Medical collections dispute (a very common Philly issue)

Philadelphia has major healthcare systems and lots of third-party billing. Medical collections can become messy because:

For a medical collections dispute, gather:

Then dispute specific inaccuracies:

C) Mixed credit file dispute (when someone else’s info lands on your report)

A mixed credit file dispute is when the bureau’s system blends information from two people with similar identifiers (similar names, family members, or similar SSNs). Red flags:

-

Addresses you’ve never lived at (especially out of state)

-

Accounts you don’t recognize but look “real”

-

Employers you’ve never worked for

How to handle it:

-

Dispute incorrect personal identifiers first (addresses, variations)

-

Then dispute the accounts that clearly don’t belong

-

Provide ID and proof of residence (lease, utility bill, etc.)

D) Incorrect personal information (quietly dangerous)

Wrong addresses and name variations can lead to denials or cause future file mixing. Dispute these items even if they don’t “hurt your score,” because they can increase confusion later.

This section is where many Philadelphia credit report errors get corrected fastest—because the dispute is grounded in documents the bureaus can verify quickly.

Identity Theft Credit Report Dispute: Philly-Focused Action Plan

If you suspect identity theft, you want a faster, more protective plan than a standard dispute. An identity theft credit report dispute should prioritize stopping new damage while you clean up the old.

Step 1: Report identity theft and create your recovery plan

The FTC’s IdentityTheft.gov is the federal starting point for reporting and recovery steps.

It provides step-by-step guidance and checklists, which can strengthen your documentation trail.

Step 2: Place protections on your credit file

Common protective steps include:

Step 3: Dispute the fraudulent accounts with each bureau

To dispute errors with Equifax Experian TransUnion related to identity theft, include:

-

Your IdentityTheft.gov report (and/or police report if you filed one)

-

A clear list of fraudulent items (account name + partial account number)

-

A request to remove fraudulent accounts and inquiries tied to them

Step 4: Notify the furnishers too

If the account came from a bank, lender, or collector, contact them directly with:

Step 5: Keep a Philly-local escalation route in your back pocket

If you’re being stonewalled, Philadelphia has local consumer-protection reporting pathways. The City of Philadelphia’s consumer threat/scam reporting page lists options, including contacting the Philadelphia Consumer Financial Protection Task Force via email at consumer.protection@phila.gov, plus state and federal complaint routes.

Identity theft disputes feel overwhelming—but when you turn it into a checklist, you regain control quickly.

Winning the Follow-Up: What to Do After “Verified” (and When to Escalate Locally)

One of the most frustrating outcomes in the credit bureau dispute process is a response that says the item was “verified” and will remain. This is exactly where a smart follow-up dispute after verification can make the difference.

First, understand what “verified” really means

“Verified” usually means:

It does not automatically mean the information is accurate in the real world. Data systems can be wrong, incomplete, or misapplied to the wrong person.

Step-by-step follow-up dispute strategy

If you get “verified,” don’t resend the same dispute. Do this instead:

1) Request more specificity

-

Dispute again, but add new evidence or a clearer explanation

-

Ask the bureau to reinvestigate based on the attached documentation

2) Dispute the data details that are easiest to prove wrong

For example:

3) Dispute with the furnisher directly

Many consumers only dispute with bureaus. But if the furnisher is the source of the error, you often need them to correct their reporting pipeline too.

4) Escalate with complaints when appropriate

If the process stalls, you can escalate through:

-

CFPB complaint process (especially if a bureau/furnisher isn’t responding appropriately)

-

Pennsylvania Office of Attorney General consumer complaint process

-

Philadelphia consumer protection reporting options (including the task force email)

Common Philly consumer mistake: escalating too early

It’s tempting to file a complaint immediately, but many disputes require that standard 30–45 day window to complete. The CFPB explicitly warns that filing too early can interfere with the process.

A strong credit report dispute Philadelphia plan is patient and persistent: follow the timeline, upgrade the evidence, and escalate strategically—not emotionally.

Credit Report Dispute Letter Toolkit + Long-Term Credit Health After the Fix

If you want maximum control, a credit report dispute letter is one of the most useful tools you can have—especially when your dispute is complex (mixed files, identity theft, stubborn collections, repeated “verified” outcomes).

What a strong dispute letter includes

Use this checklist format:

-

Your info: full name, DOB, current address, partial SSN

-

Bureau name + address: (the bureau you’re writing)

-

Date

-

Subject line: “Credit Report Dispute”

-

Disputed item details: creditor/collector name, partial account number, report date

-

Statement of dispute: what’s wrong + why (keep it short)

-

Requested resolution: delete/correct/update

-

Attachments list: ID proof + supporting documents

-

Signature

Sample credit report dispute letter (copy/paste template)

(Customize the bracketed areas.)

Hello,

I am writing to dispute inaccurate information on my credit report. The item(s) listed below are incorrect and I am requesting an investigation and correction or deletion.

Disputed item:

-

Creditor/Collector: [Name]

-

Account number (partial): [XXXX]

-

Error: [Explain in 1–2 sentences]

-

Requested update: [Delete / Correct to ______ / Update status to ______]

Supporting documents attached:

-

Proof of identity: [Driver’s license/ID]

-

Proof of address: [Utility bill/lease]

-

Evidence: [Payment proof, statements, IdentityTheft.gov report, EOB, etc.]

Please send me the results of your investigation in writing and provide an updated copy of my report if changes are made.

Sincerely,

[Your full name]

[Your current address]

[Your phone/email]

After disputes: how to keep your credit healthy long-term

Correcting errors is powerful, but the long-term benefits come from maintaining strong habits:

-

Pay on time (set autopay + reminders)

-

Keep credit card utilization manageable

-

Avoid unnecessary hard inquiries

-

Monitor reports regularly for new errors

This is where “credit repair” becomes credit resilience: fewer future surprises, better approvals, and less stress.

A quick word on getting help

If you’ve tried to dispute credit report errors in Philadelphia and keep hitting “verified” responses, or you’re dealing with complex issues like a mixed credit file dispute or identity theft credit report dispute, professional guidance can save time and help you organize your evidence and dispute strategy. Credit Repair Associates can be a helpful option for consumers who want hands-on Philadelphia credit repair dispute help while they work toward stronger credit outcomes.

FAQs

1) How do I dispute credit report errors in Philadelphia?

To dispute credit report errors in Philadelphia, start by pulling your reports from Equifax, Experian, and TransUnion. Identify the exact items that are inaccurate, gather proof (statements, receipts, letters, ID documents), then submit a credit report dispute Philadelphia request online or by mail. Keep copies of everything and track the dispute timeline so you can follow up if the item is “verified” without being corrected.

2) How long do credit report disputes take in Philadelphia?

In most cases, credit bureau investigations take about 30 days, and some disputes may take up to 45 days depending on the situation and how the dispute was submitted. If you submit additional information after filing, it can also affect timing. Always save your confirmation or certified mail receipt so you can track when the bureau received your dispute.

3) Should I dispute errors with Equifax, Experian, and TransUnion separately?

Yes. Each bureau maintains its own file, so if the same Philadelphia credit report errors appear on more than one bureau, you typically need to dispute errors with Equifax Experian TransUnion individually. A correction at one bureau doesn’t automatically guarantee the other bureaus will update, so it’s smart to check all three reports after results come back.

4) What should I include in a credit report dispute letter?

A credit report dispute letter should include your full name, date of birth, current address, and the last four digits of your SSN, plus the account details (creditor name and partial account number). Clearly explain what is inaccurate, what you want changed, and attach supporting documents (proof of payment, statements, identity theft reports, insurance EOBs for medical collections dispute, etc.). Keep the letter short, factual, and organized.

5) Can I dispute an inaccurate collection account in Philadelphia?

Yes. If you need to dispute inaccurate collection account reporting, focus on verifiable issues like incorrect balance, wrong dates, duplicate collections, or accounts that don’t belong to you. Provide documentation when possible and consider disputing with both the credit bureau and the company reporting the debt to strengthen your position.

6) How do I handle an identity theft credit report dispute?

For an identity theft credit report dispute, document the fraud first (for example through IdentityTheft.gov), then dispute the fraudulent accounts and inquiries with each bureau. Include your identity theft report and proof of identity/address to support removal. You may also need to contact the lenders or collectors directly so they stop reporting the account and correct their records.

7) What if my credit report dispute is marked “verified” but still wrong?

If the bureaus respond that the item was verified, don’t send the same dispute again. A follow-up dispute after verification is strongest when you add new evidence, clarify the exact data point that’s wrong (dates, balance, ownership), and dispute directly with the furnisher (the company reporting). If the issue still isn’t resolved, filing a complaint with the CFPB or your state consumer office may be appropriate.

by administrator | Feb 10, 2026 | Blogs

When people think about money goals—buying a home, getting a reliable car, renting a better apartment, even lowering insurance costs—credit is often the silent gatekeeper. If you’ve ever been surprised by a denial, a high interest rate, or a requirement for a large deposit, your credit profile may be the reason.

The good news: credit repair in Pennsylvania doesn’t have to be mysterious or intimidating. At its core, Pennsylvania credit repair is about two things:

-

Accuracy (making sure your credit reports reflect correct, verifiable information), and

-

Strategy (building habits and account management routines that improve scores over time).

This guide is designed for real people who want a clear, actionable plan—whether you’re dealing with late payments after a tough year, collections you don’t recognize, high utilization, or errors that are dragging your score down. You’ll learn how credit reporting works, how disputes actually get resolved, what to watch out for, and how to maintain strong credit once your reports are cleaned up.

And importantly, we’ll cover credit repair laws in Pennsylvania (and credit repair laws PA consumers should know), so you can protect yourself if you decide to use credit repair services Pennsylvania residents may encounter online or locally.

Why Credit Repair in Pennsylvania Matters More Than You Think

Your credit doesn’t only matter when you apply for a credit card. It can influence major life decisions and everyday costs—often in ways people don’t expect until it’s too late. That’s why credit repair in Pennsylvania is about more than boosting a number; it’s about improving financial options.

Here are a few common ways credit impacts Pennsylvania consumers:

-

Mortgages and homebuying: Better credit usually means better pricing. Even small rate differences can translate into thousands over the life of a loan.

-

Auto loans: A lower score can mean higher monthly payments or being required to use a co-signer.

-

Renting: Landlords may check credit to assess reliability and may charge higher deposits for weaker profiles.

-

Utilities and cell phone plans: Many providers use credit-based decisions for deposits.

-

Employment screening: Some employers use credit reports in hiring decisions where permitted and relevant (typically not your score, but the report).

-

Insurance pricing (in many states): In some situations, insurance companies may use credit-based insurance scores as part of pricing models (rules vary by product and state).

The real challenge is that credit problems often compound. A single late payment can trigger a higher interest rate, which increases balances faster, which pushes utilization up, which can lower scores further—making it harder to refinance or consolidate. The earlier you address issues, the easier how to fix credit in Pennsylvania becomes.

Also, many consumers assume credit repair is “removing negative items.” In reality, Pennsylvania credit repair is often about removing incorrect or unverifiable information and then rebuilding. Accurate negative items may remain until they age off, but your score can still improve significantly through better utilization, on-time history, and smart account structure.

Think of your credit as a financial résumé. If there are errors on your résumé, you correct them. If there are weak spots, you strengthen your experience. That’s the mindset that makes credit repair services Pennsylvania consumers pursue either DIY or professional help—but always with a plan.

Understanding Credit Reports and Scores: The Foundation of Pennsylvania Credit Repair

Before you dispute anything, it helps to know what you’re looking at. Your credit report is not one single report; it’s typically a file maintained by multiple credit bureaus (the “big three” are commonly referenced). Each bureau can have slightly different information because not every lender reports to all bureaus and timing can vary.

A credit report generally includes:

-

Personal information: Name variations, addresses, employers (errors here can signal mixed files).

-

Trade lines (accounts): Credit cards, auto loans, mortgages, student loans—showing balances, limits, payment history, and status.

-

Collections: Debts placed with collection agencies (sometimes duplicates happen).

-

Public records: Some public record reporting has changed over time; always verify accuracy.

-

Inquiries: Hard inquiries (applications) and soft inquiries (checks that don’t affect lending decisions the same way).

Your credit score is a separate calculation based on the data in the report. While scoring models differ, most reward similar behaviors:

-

Paying on time

-

Keeping revolving utilization low

-

Maintaining longer account history

-

Limiting new credit applications

-

Having a healthy mix of accounts

Actionable tip for credit repair in Pennsylvania:

Start by pulling and organizing your reports so you can compare bureau-to-bureau. Create a simple tracking list of:

-

Account name

-

Account number (masked)

-

Reported balance and limit

-

Payment status (current, late, charged off)

-

Date of first delinquency (if negative)

-

Notes: “wrong balance,” “not mine,” “duplicate,” “paid but still open,” etc.

Example:

If one bureau shows a paid collection as unpaid, or shows the wrong date of last payment, your dispute strategy changes. That’s why how to fix credit in Pennsylvania starts with documentation and consistency.

Also, be careful with “credit monitoring” alerts alone. Monitoring is useful for catching changes, but it may not show you the full detail you need for disputes. For Pennsylvania credit repair, you want the full report details so you can challenge inaccurate reporting precisely.

The Credit Repair Process: A Step-by-Step Plan for How to Fix Credit in Pennsylvania

A strong credit repair in Pennsylvania plan is structured. Random disputes and guesswork often waste time and can even backfire if you dispute accurate information without a clear reason.

Here’s a clean, consumer-friendly process:

Step 1: Gather reports and proof

Pull your credit reports and gather supporting documents:

-

Driver’s license or state ID

-

Utility bill/bank statement (proof of address)

-

Account statements, payment confirmations, settlement letters

-

Identity theft reports (if applicable)

Step 2: Identify what’s hurting you most

Not all negative items affect your score equally. Prioritize:

-

High revolving utilization

-

Recent late payments

-

Collections (especially recent)

-

Charge-offs with ongoing balances

-

Errors like accounts that don’t belong to you

Step 3: Separate “dispute” items from “rebuild” items

For Pennsylvania credit repair, your plan should include both:

-

Dispute track: inaccurate, incomplete, or unverifiable items

-

Rebuild track: utilization reduction, on-time streak, account optimization

Step 4: Dispute with a goal (not “delete everything”)

The best disputes are specific:

-

“This balance is inaccurate; attached statement shows correct balance.”

-

“This account is not mine; attached ID and address proof included.”

-

“This collection is duplicated; same debt appears twice with different account numbers.”

Step 5: Create a 90-day score improvement routine

Even while disputes are pending, you can move the score needle:

Weekly (15 minutes):

-

Check balances before statement close

-

Pay revolving accounts down strategically

-

Confirm autopay is active

Monthly (30 minutes):

-

Review reports/monitoring changes

-

Update your dispute tracker

-

Plan next month’s utilization target

Step 6: Track outcomes and escalate correctly

If results come back “verified” but you have documentation that contradicts the reporting, your next step may be to dispute with additional evidence or dispute directly with the furnisher in certain situations.

This structured approach is the backbone of how to fix credit in Pennsylvania without getting overwhelmed. It’s also what reputable credit repair services Pennsylvania consumers look for should follow—clear steps, documentation, and measurable progress.

How to Dispute Errors and Negative Items on Your Credit Report (The Right Way)

Disputing is where many consumers either make rapid progress—or lose momentum. Under the federal Fair Credit Reporting Act (FCRA), consumer reporting agencies must investigate disputes, generally within 30 days (with limited extensions under certain conditions).

What you can dispute

You can typically dispute information that is:

-

Inaccurate (wrong balance, wrong dates, wrong status)

-

Incomplete (missing details that change the meaning)

-

Not yours (mixed files, identity theft)

-

Unverifiable (cannot be validated through proper investigation)

The “clean dispute” formula (works well for credit repair in Pennsylvania)

Use a short, organized packet:

-

Cover letter (one page, bullet points)

-

Copy of ID + proof of address

-

Highlighted report page(s) showing the error

-

Supporting documents (statements, receipts, letters)

Tip: Dispute one “theme” per letter when possible. For example, don’t combine identity theft disputes with a utilization issue and a goodwill request. Clear disputes get clearer investigations.

Dispute routes you can use

-

Dispute with the credit bureau

This is the most common route. You’re asking the bureau to reinvestigate and correct/delete inaccurate reporting per FCRA procedures.

-

Direct dispute with the furnisher (the company reporting the data)

In some cases, you can dispute directly with the data furnisher, which is required to conduct a reasonable investigation when it receives a proper dispute notice.

What to do with these common negative items

-

Late payments: If the late is accurate, disputes usually won’t remove it. You may focus on rebuilding, or try a goodwill approach (not guaranteed).

-

Collections: Verify it’s yours, verify the balance, verify duplicates. If it’s paid, confirm the reporting is accurate and consistent.

-

Charge-offs: Confirm dates, balances, and whether it’s being reported as charged off correctly each month.

-

Accounts not yours: Act quickly, document thoroughly. If identity theft is involved, consider filing official reports and placing fraud alerts or freezes.

Mistake to avoid

Don’t send vague letters like “This is not accurate, please delete.” That’s one reason disputes fail. Strong Pennsylvania credit repair disputes are specific, documented, and easy to evaluate.

Credit Repair Laws in Pennsylvania: What Consumers Should Know Before Hiring Help

If you’re considering credit repair services Pennsylvania consumers see advertised online, it’s important to understand the rules that protect you. Credit repair is regulated at both the federal and state levels, which is why credit repair laws in Pennsylvania and credit repair laws PA are such a big deal.

Federal protections (CROA)

The federal Credit Repair Organizations Act (CROA) restricts deceptive practices, requires disclosures, requires written contracts, and generally prohibits charging upfront before services are performed.

This matters because many scams rely on:

-

Promising a “new credit identity” or “fresh file”

-

Guaranteeing deletions

-

Charging large upfront fees while doing little work

-

Advising you to dispute accurate information dishonestly

CROA also requires certain consumer disclosures before you sign a contract.

Pennsylvania protections (Credit Services Act + consumer protection law)

Pennsylvania has its own rules that regulate “credit services” and prohibit certain practices. Pennsylvania’s Credit Services Act addresses prohibited activities and includes provisions related to consumer information requirements and restrictions around payment before performance (with specific compliance options such as bonding/trust arrangements for certain situations).

Pennsylvania’s broader Unfair Trade Practices and Consumer Protection Law (UTPCPL) is also relevant because it targets unfair or deceptive business practices and is enforced by state authorities, with private remedies in some cases.

What to look for before hiring any Pennsylvania credit repair help

Use this consumer checklist:

-

They don’t guarantee results (no one can promise deletions)

-

They explain your rights and provide written disclosures

-

They use written contracts and clear timelines

-

They don’t encourage dishonest disputes or “new identities”

-

They can explain the difference between disputing errors and rebuilding credit

Understanding credit repair laws PA consumers benefit from helps you avoid paying for false promises—and helps you choose support that actually follows the rules.

Rebuilding Credit After Disputes: Habits That Improve Scores Long-Term

Disputes can remove errors, but rebuilding is what creates lasting results. The strongest credit repair in Pennsylvania outcomes usually come from pairing clean-up with consistent habits.

The biggest score-movers you can control

1) On-time payments (every month)

Payment history is the backbone of scoring. If you’ve struggled, consider:

-

Autopay for minimum payments

-

Calendar reminders for due dates

-

Paying bi-weekly (helps cash flow and reduces missed payments)

2) Credit utilization (especially revolving)

Utilization can change your score quickly. Try these practical tactics:

-

Pay balances before the statement closing date (not just the due date)

-

Spread balances across cards (instead of maxing one)

-

Request credit limit increases cautiously (and only if spending won’t rise)

3) Account structure and age

Avoid closing older accounts without a reason. Older accounts can help average age and available credit.

A simple 3-part rebuild plan for how to fix credit in Pennsylvania

-

Stabilize: Stop late payments. Reduce utilization to a manageable level.

-

Strengthen: Add positive payment history (secured card or credit-builder loan if needed).

-

Optimize: Keep utilization low month-to-month, limit hard inquiries, and maintain a healthy mix.

Example: A realistic rebuild timeline

-

Month 1–2: Set autopay + reduce utilization by 10–20%

-

Month 3–4: Add a secured card (if needed) + keep balances low

-

Month 5–6: Continue on-time streak; re-check reports for accuracy and updates

This is the “unsexy” part of Pennsylvania credit repair, but it’s the part that keeps scores strong long after disputes are done.

Common Credit Repair Mistakes (and How Pennsylvania Consumers Can Avoid Them)

If you want credit repair in Pennsylvania to work, avoid the patterns that cause most people to stall.

Mistake #1: Disputing everything at once

Mass disputes can lead to confusion and weak investigations. Instead:

Mistake #2: Ignoring utilization while waiting on disputes

Waiting is expensive in score terms. Even if disputes take 30–45 days, utilization and on-time payments can improve your score during that time.

Mistake #3: Falling for guarantees and “quick fixes”

If you see:

Mistake #4: Not keeping records

Keep a folder (digital or paper) with:

Mistake #5: Closing accounts impulsively

Closing an account can raise utilization and reduce available credit. Consider a strategy first—especially if the account is old or has a high limit.

Mistake #6: Applying for new credit repeatedly

Multiple hard inquiries and new accounts can temporarily lower scores. Apply intentionally, not emotionally.

Avoiding these mistakes is one of the fastest ways how to fix credit in Pennsylvania becomes less stressful and more predictable—whether you’re doing it yourself or evaluating credit repair services Pennsylvania companies.

Conclusion: Credit Repair Pennsylvania Is a Process—But It’s a Powerful One

The best way to think about Pennsylvania credit repair is as a two-track system:

-

Correct what’s wrong (errors, duplicates, inaccurate reporting), and

-

Build what’s right (on-time payments, low utilization, stable accounts).

When you understand how disputes work, what documentation matters, and what credit repair laws in Pennsylvania (and credit repair laws PA) protect you from, you’re far less likely to get scammed or waste months spinning your wheels.

If you want to handle credit repair in Pennsylvania on your own, use the step-by-step process in this guide and track everything. And if you prefer professional support, Credit Repair Associates may be an option for consumers who want help reviewing reports, preparing disputes correctly, and staying consistent with a long-term improvement plan.

FAQ section

1) What is credit repair in Pennsylvania?

Credit repair in Pennsylvania is the process of reviewing your credit reports, disputing inaccurate or unverifiable items, and building positive credit habits (like on-time payments and low utilization) to improve your credit profile over time.

2) How do I fix my credit in Pennsylvania fast?

The fastest improvements usually come from lowering credit card utilization, setting up autopay to prevent late payments, and disputing clear errors. “Fast” still typically means weeks to months, not days—especially for disputes.

3) What are the first steps for Pennsylvania credit repair?

Start by pulling your credit reports, listing issues by bureau, gathering documents (ID, proof of address, statements), and prioritizing high-impact problems like utilization, recent late payments, and accounts that aren’t yours.

4) How long does a credit dispute take?

Many disputes are resolved within about 30 days, though timing can vary based on the type of dispute and how it’s submitted. Keep records and track outcomes.

5) Can I dispute negative items that are accurate?

You can dispute items you believe are inaccurate, incomplete, or unverifiable. If an item is accurate and properly documented, it may remain until it naturally ages off your report.

6) What credit report errors are most common?

Common errors include accounts that don’t belong to you, incorrect balances or limits, wrong payment status, duplicated collections, incorrect dates, and mixed-file issues.

7) How do I dispute errors correctly?

Use a clear letter, include copies of ID and proof of address, highlight the error on your report, attach supporting documents, and dispute one theme at a time for cleaner investigations.

8) Should I dispute online or by mail?

Online can be quicker, but many consumers prefer mail for better documentation and attachments. Whatever method you choose, keep copies of everything you send.

9) What are credit repair laws in Pennsylvania?

Credit repair laws in Pennsylvania (and credit repair laws PA) include consumer protections that regulate credit services and prohibit deceptive practices. You should also know federal protections under CROA and FCRA.

10) Is it legal to hire credit repair services Pennsylvania companies?

Yes, it can be legal—if the company follows applicable laws, provides required disclosures, uses written agreements, and does not engage in deceptive claims or “guaranteed” deletions.

11) Can a credit repair company remove late payments?

If late payments are accurate, they usually cannot be removed through disputes. Some consumers attempt goodwill requests with creditors, but results aren’t guaranteed.

12) Do paid collections help my credit?

Paid collections can be better than unpaid from a lender-risk perspective, but scoring impact depends on the scoring model used. Accuracy and proper reporting still matter.

13) What’s the biggest thing that improves a credit score after repair?

Consistency: on-time payments, lower revolving utilization, fewer new hard inquiries, and stable account management over time.

14) Will checking my credit hurt my score?

Checking your own credit is typically a soft inquiry and does not hurt your score. Hard inquiries usually come from applying for new credit.

15) What is the best utilization target when rebuilding credit?

Many consumers aim for low utilization, often under 30%, and even lower if possible for stronger scoring results—especially on revolving credit cards.

16) Should I close old credit cards after credit repair?

Not automatically. Closing old cards can reduce available credit and raise utilization. Evaluate fees, usage, and credit age before closing accounts.

17) How do I rebuild credit if I can’t get approved?

Options may include a secured card, becoming an authorized user (with caution), or a credit-builder loan. The best option depends on your report and budget.

18) What mistakes slow down credit repair in Pennsylvania?

Common mistakes include disputing everything at once, sending vague disputes, ignoring utilization, applying for too much new credit, and failing to keep records.

19) What documents should I save during the credit repair process?

Keep dispute letters, reports before/after, proof of delivery (if mailed), responses from bureaus or furnishers, and any supporting statements or receipts.

20) When should I consider professional help?

If you’re overwhelmed, dealing with identity theft or mixed files, or you want help organizing disputes and strategy, professional guidance can be useful—just vet providers carefully.

References

by administrator | Feb 3, 2026 | Blogs

The Fair Credit Reporting Act (FCRA): Why It Exists and What It Protects

If you’ve ever applied for a credit card, apartment, car loan, cell phone plan, or even certain jobs, you’ve felt the power of your credit report—sometimes without realizing it. The Fair Credit Reporting Act (FCRA) is the federal law designed to keep that power from being used against you unfairly. At its core, the FCRA is about consumer rights + protections in a system where mistakes can be expensive and privacy matters.

The FCRA was created to promote the accuracy, fairness, and privacy of credit reports. That phrase is more than legal language—it’s the “why” behind the law. Credit reporting agencies (often called “credit bureaus”) collect and sell information about how people manage credit. Because lenders and other companies rely on that information to make decisions, the FCRA sets rules for how credit data can be gathered, shared, and corrected.

So what does that mean for you in real life?

-

It means you have Fair Credit Reporting Act rights to challenge inaccurate information.

-

It means you have consumer rights under FCRA to know when your credit report is used against you.

-

It means credit bureaus and companies that report information (often called “furnishers” or “data furnishers”) have responsibilities—not just you.

Another major piece of the story is that the FCRA has been strengthened over time. A key amendment came with the Fair and Accurate Credit Transactions Act (FACTA), which expanded consumer access and identity-theft protections—most famously by giving you the right to a free annual credit report from each of the major credit bureaus.

Why should someone focused on credit repair care about any of this? Because credit repair isn’t magic. It’s a process of using your rights—especially your right to dispute inaccurate, incomplete, or unverifiable information—so your report reflects your real history. When your credit report is more accurate, your credit score often improves as a result.

Think of the FCRA like the rulebook for the credit reporting world. When you know the rules, you stop guessing and start taking targeted steps—with confidence that the law backs you up.

What’s Actually Inside a Credit Report—and Why Credit Repair Starts Here

Before you can fix a credit report, you have to understand it. Most people think of credit repair as “removing negative items,” but the truth is more practical: credit repair starts with making sure your report is correct and complete—and that it reflects the accuracy, fairness, and privacy of credit reports the FCRA aims to protect.

A typical credit report includes:

-

Personal information (name variations, addresses, employers)

-

Account histories (credit cards, loans, mortgages, student loans)

-

Payment history (on-time payments, late payments, charge-offs)

-

Collections and sometimes public record data (depending on bureau practices and data sources)

-

Credit inquiries (hard inquiries tied to applications, and soft inquiries tied to checks)

Here’s why this matters: a small error in one area can snowball into bigger consequences. An incorrect late payment could raise your interest rates. A mixed file (where someone else’s account appears on your report) can make you look riskier than you are. Even outdated personal information can be a red flag that your file is being merged incorrectly.

Credit repair consumers often focus only on the obvious negative items. But a thorough approach checks for:

-

Inaccurate balances or credit limits (affects utilization)

-

Wrong account statuses (open vs. closed, paid vs. unpaid)

-

Duplicate collections (same debt reported multiple ways)

-

Incorrect dates (late payment dates, “date opened,” first delinquency)

-

Unauthorized inquiries (privacy and permissible access issues)

This is where consumer rights + protections come in. The FCRA doesn’t promise you a “perfect” score—it gives you a system to correct reporting that is wrong, incomplete, or can’t be verified. And when reporting is corrected, many people see score improvement because the score is calculated from what’s on the report.

A helpful mindset shift: credit repair is not about arguing your way out of legitimate debt. It’s about ensuring the data used to judge you is fair and accurate. In that sense, credit repair is a form of financial self-defense—using consumer rights under FCRA to prevent errors from limiting your options.

Actionable tip: treat your credit report like a financial medical chart. Don’t skim it. Read every section, line by line, and compare it to your own records (statements, payment confirmations, settlement letters, account closure letters). The goal is simple: the report should match reality.

Your FCRA Rights in Action: Access, Privacy, and “Permissible Purpose”

Most people learn about the FCRA when something goes wrong—an unexpected denial, a higher rate than promised, or a collection account they don’t recognize. But your Fair Credit Reporting Act rights aren’t only “emergency tools.” They’re everyday protections that help you control your financial identity.

Your right to access your credit report

Thanks to FACTA, you’re entitled to a free annual credit report from each of the nationwide credit bureaus. The official site set up for this purpose is AnnualCreditReport.com.

This matters because you can’t dispute what you don’t see. Regularly pulling your reports helps you catch problems early—before they cost you approvals, deposits, or job opportunities.

Your right to privacy and limited access

The FCRA limits who can access your report and why. In legal terms, this is about permissible purpose—a company generally needs a valid reason (like evaluating a credit application) to obtain your consumer report.

This is a big part of the “privacy” in the accuracy, fairness, and privacy of credit reports promise. Your report isn’t supposed to be open-season for anyone who’s curious.

Your right to accurate reporting and to challenge errors

This is the heart of credit repair: consumer rights under FCRA include the ability to challenge information that is inaccurate, incomplete, or can’t be verified. When you use these rights properly, you’re not asking for a favor—you’re initiating a regulated process.

Your right to transparency when your report hurts you

If your credit report plays a role in a negative decision, the law gives you pathways to learn what happened and what to do next (we’ll cover adverse action notices in detail later).

Practical ways to use these rights right now:

-

Pull all three reports (not just one bureau) and compare them. Differences are common.

-

Identify any account you don’t recognize, any late payment you dispute, and any balance that looks wrong.

-

Make a “proof folder” (digital or paper) with statements, letters, payment receipts, and identity documents.

-

Track your timeline. Credit repair is partly about organization—and partly about knowing the rules.

When you understand these protections, credit stops feeling like a mysterious score controlled by someone else. The FCRA is your reminder that you have rights, and the system has responsibilities.

How to Dispute Errors on a Credit Report: The Credit Report Dispute Process Step-by-Step

If you’re trying to dispute errors on credit report data, you’ll get better results by treating it like a documented process—not a quick complaint. The FCRA lays out the framework for a credit report dispute process that credit bureaus and furnishers must follow, and it’s one of the most powerful consumer rights + protections available.

Step 1: Identify exactly what is wrong

Be specific. “This is inaccurate” is weaker than “The account shows a 60-day late in May 2024, but my statement and bank record show the payment cleared on April 28, 2024.”

Create a dispute list with:

-

Bureau (Equifax/Experian/TransUnion)

-

Account name and number (partial if needed)

-

The inaccurate detail (date, status, balance, payment history)

-

The correction you’re requesting

-

The documents that support your claim

Step 2: Decide where to dispute

You can dispute with the credit bureau, and in many situations also with the furnisher that reported the information. The FCRA/Regulation V also addresses “direct disputes” in certain contexts.

For most consumers, starting with the bureau is common because bureaus must route the dispute to the furnisher for investigation.

Step 3: Submit your dispute with supporting proof

Your goal is to make it easy to verify your position. Attach only what’s relevant (avoid sending your whole life). Examples:

-

Billing statements

-

Proof of payment (bank confirmation)

-

Identity documents (for mixed files/identity theft issues)

-

Letters showing an account was closed/paid/settled

-

Police/identity theft reports when appropriate

Step 4: Understand the FCRA dispute process timeline

Once your dispute is received, the credit bureau must investigate within 30 days in most cases.

That’s why you’ll often hear credit repair professionals talk about “rounds” of disputes—timelines matter.

Step 5: Review results and your updated report

At the end of the investigation, the bureau must tell you the outcome and provide results. If something is corrected or deleted, make sure it updates across all bureaus where it appears.

Step 6: Escalate intelligently if needed

If an item returns as “verified” but your evidence is strong, don’t panic. You may:

-

Request more detail (keep records of everything)

-

Dispute again with new or clearer documentation

-

Dispute with the furnisher directly (where applicable)

-

Add a consumer statement (last resort—can be ignored by scoring models)

The biggest advantage consumers have is the law-backed structure. When you follow a disciplined FCRA dispute process, you turn a frustrating situation into a trackable, winnable workflow.

Disputes + Timelines: What the 30-Day Rule Means and How to Use It Strategically

The phrase “Disputes + timelines” may sound boring—until you realize it’s where many credit repair attempts succeed or fail. Timing affects everything: how long negative information continues to impact you, when you can reapply for credit, and whether you can build momentum with score improvement.

The key timeline: 30 days (sometimes a bit longer)

Under the FCRA, the bureau generally has 30 days to complete a reinvestigation after receiving your dispute.

There’s an important nuance: the timeline can be extended if you send additional relevant information during the investigation window (the statute allows a limited extension).

That’s why the practical guidance is: send a complete dispute package upfront whenever possible.

So when you hear “credit bureau must investigate within 30 days,” think: “I need to track my dates, keep my receipts, and avoid last-minute add-ons.”

Why disputes sometimes take 30–45 days in the real world

Consumers often experience a “30–45 day” rhythm because of mailing time, processing time, and allowed extensions. Many credit education resources reference this general window, but the legal anchor is the FCRA reinvestigation period.

How to use timelines to your advantage

Here are practical strategies credit repair consumers can use:

-

Dispute in batches. Don’t dispute 20 items at once if you can’t track them.

-

Prioritize high-impact items first: recent lates, high balances, collections, and errors tied to identity/mixed files.

-

Calendar your follow-ups: mark the date the bureau received your dispute and the expected resolution window.

-

Avoid “credit repair noise”: sending repeated disputes with no new info can weaken your case.

-

Keep a paper trail: screenshots, certified mail receipts, confirmation numbers—whatever applies to your submission method.

Why timelines matter for score improvement

Even when corrections are coming, your score doesn’t update because you “started a dispute.” It updates when the data changes—deleted, corrected, or updated. So disputes are best paired with positive actions during the waiting period, such as:

-

Paying revolving balances down (utilization)

-

Keeping accounts current (payment history)

-

Avoiding new unnecessary hard inquiries

Credit repair works best when you treat it like a project: plan the work, work the plan, and respect the clock built into the credit report dispute process.

Denied Credit? Understand Adverse Action Notices and Your “Free Report in 60 Days” Rights

Getting declined can feel personal. But under the law, a denial can also be a doorway to information—if you know what to look for. When a lender, insurer, employer, or landlord uses a consumer report to make a negative decision, you may receive an adverse action notice credit report consumers often overlook. These notices connect directly to Fair Credit Reporting Act rights and can help you act fast.

What is an adverse action notice?

An adverse action notice is a disclosure explaining that a negative decision was made (or terms were worsened) based partly on information in a consumer report. The notice is meant to tell you:

-

That your credit report influenced the decision

-

Which credit bureau supplied the report

-

That the bureau didn’t make the decision (they provided data)

-

How to obtain your report and dispute inaccurate information

Regulators and compliance guidance emphasize that adverse action disclosures exist so consumers can understand and respond to the reasons for denial.

Your “free report in 60 days” right after adverse action

One of the most practical protections: if you receive an adverse action notice, you generally have the right to request a free credit report within 60 days after adverse action. This is a critical tool for people who were denied credit due to credit report rights—because it gives you immediate access to the data that hurt you, so you can dispute errors quickly.

How to use an adverse action notice strategically

If you’re denied:

-

Get the notice and read it carefully. It should name the bureau used.

-

Request your report right away using the bureau information in the notice.

-

Compare the denial reasons to the report details.

-

Dispute inaccuracies immediately using the FCRA dispute process (with proof).

-

Reapply only when the data changes or you’ve improved the underlying risk factors.

Why this matters for credit repair consumers